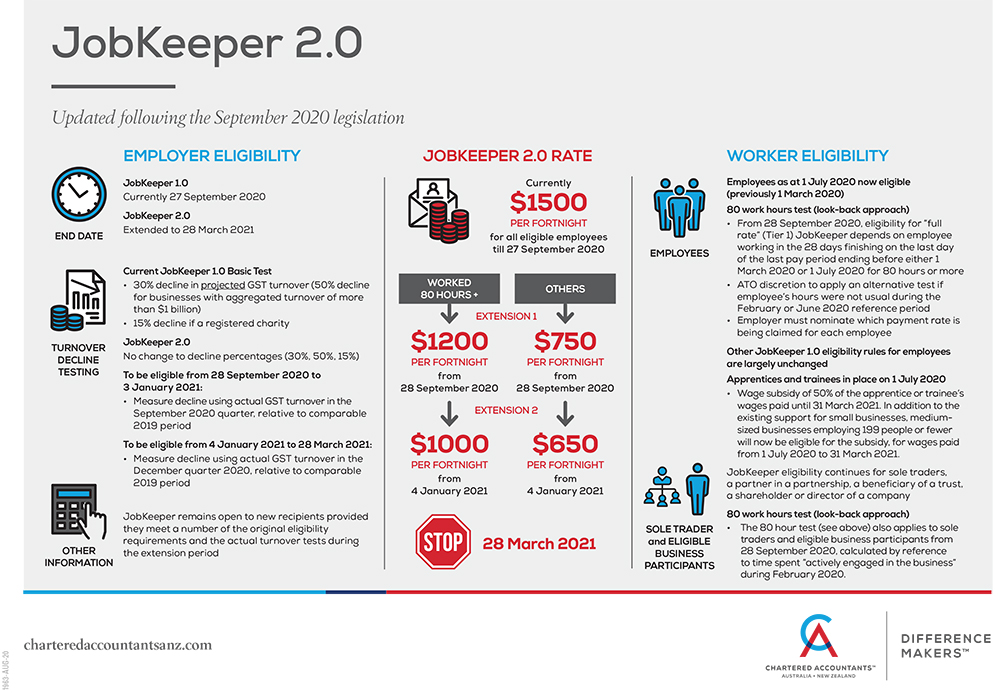

Extended Scheme – 13 more fortnights

The current job keeper schemes ended on 27th September 2020.

Job Keeper 2.0 started 28th September 2020 and will run until 28th March 2021.

It is made up of two Extension periods:

28th September 2020 to 3rd January 2021

4th January 2021 to 28th March 2021

If you are currently enrolled in Job Keeper 1.0, then you do not need to re-enrol. But you do need to re-test and meet the eligibility tests for each Extension period. Each extension period is independent of the other, so you can qualify for either or both. If you have never received jobkeeper in the past, you can now check to see if you are eligible for the extension period.

Eligible Employees from 1st July 2020

Previously only employees on your books at 1st March 2020 were eligible employees for Jobkeeper purposes. Now recheck your payroll records.

If they were a permanent employee whether full or part time on 1st July 2020, they are now an eligible employee. For casuals, they are considered to be a long-term casual employee where on 1 July 2020, you employed them on a regular and systematic basis for a period of 12 months. (ie from 2/7/19 to 1/7/20)

Payment rates

| Extension Period 1 | Tier 1 Averaged 20 hours or more per week in the test period | Tier 2 Averaged less than 20 hours per week in the test period |

| 1. 28th September 2020 to 3rd January 2021 | $1200 per fortnight | $750 per fortnight |

| 2. 4th January 2021 to 28th March 2021 | $1000 per fortnight | $650 per fortnight |

Test Period:

This refers to the two (2) fortnights either before 1st March 2020 or 1st July 2020.

Basically you tally up the hours for the 4 weeks and average it to see if you meet or fall short of the 20 hours per week. This allows smoothing as especially casuals can work different shifts each week and hours will vary. When looking at pay cycles, it is completed pay cycles.

https://www.ato.gov.au/General/JobKeeper-Payment/Payment-rates/80-hour-threshold-for-employees/

The Decline in Turnover Test

The decline in turnover test remains at 30% and over. But rather than being based on projected GST turnover, it is based on actual GST turnover.

For extension period 1 – you need to compare September QTR BAS 2020 with September QTR BAS 2019

For extension period 2 – you need to compare December QTR BAS 2020 with December QTR BAS 2019

For each comparable period, compare your actual GST turnover, which would be represented by label G1 on your GST return (using inclusive of GST) number.

The same exclusions apply ie exclude job keeper received and Cash flow boost received. Alternate tests still exist for those entities who may not have a comparable period or who may have circumstances which skew the comparatives.

Please contact us if you have any questions regarding your eligibility.

Some further guidelines from Chartered Accountants below:

Other references:

ATO guideline: https://www.ato.gov.au/General/JobKeeper-Payment/In-detail/JobKeeper-extension-what-you-need-to-do-as-a-business-or-not-for-profit/

Alternate tests: https://www.ato.gov.au/General/JobKeeper-Payment/In-detail/Actual-decline-in-turnover-test/?anchor=Alternativeturnovertest#Alternativeturnovertest

80 Hour Threshold: https://www.ato.gov.au/General/JobKeeper-Payment/Payment-rates/80-hour-threshold-for-employees/